California is at the forefront of climate regulation in the US, and one of the most important agencies driving this progress is the California Air Resources Board (CARB). The state’s climate disclosure laws, shaped by Senate Bill 253 and Senate Bill 261, together with Senate Bill 219, form the foundation of California’s approach to corporate climate accountability.

CARB’s greenhouse gas (GHG) reporting rules are detailed and mandatory for any large enterprise operating in or doing business with California. These requirements are part of California’s broader Climate Accountability Package, which aims to increase transparency and expand corporate disclosure obligations.

Failing to comply can result in penalties, reputational harm, and delays in achieving ESG goals. Companies are also under growing pressure to improve voluntary carbon market disclosures and align with international standards such as the Corporate Sustainability Reporting Directive (CSRD).

This guide outlines CARB’s reporting requirements, including who must comply, what data to report, and the key risks associated with non-compliance.

What is the California Air Resources Board (CARB)?

The California Air Resources Board (CARB) is the state agency tasked with protecting public health by reducing air pollution and addressing climate change. Established in 1967, it remains one of the world’s most progressive and influential environmental regulators.

CARB develops and enforces rules that target greenhouse gas emissions, air quality, and the adoption of clean technology. In addition, this agency issues draft regulations for public comment, and these drafts are shaped by input from frameworks such as the Task Force on Climate-Related Financial Disclosures (TCFD).

Its frameworks, including California’s reporting requirements, are specifically designed to support the state’s ambitious climate objectives, including achieving carbon neutrality by 2045.

Why CARB matters for climate disclosure laws

For enterprises, CARB requirements are more than a compliance exercise. They set the standard for how emissions should be measured and reported. California's climate disclosure laws, including SB 253, SB 261 and SB 219, are among the nation's most comprehensive and are often compared to other frameworks like the SEC's climate disclosure rules. The development of these laws involves significant public input, including public workshops hosted by regulatory agencies, which allow stakeholders to provide feedback and help shape the final regulations.

As California is a global leader in climate regulation, CARB’s frameworks are often mirrored by other states and countries. As a result, enterprises must navigate varying regulatory requirements and face significant compliance burdens as they adapt to different reporting standards across jurisdictions.

This means that compliance with CARB ensures access to the California market and prepares enterprises for broader regulatory shifts worldwide. However, ongoing regulatory uncertainty and frequent updates to programme rules, templates and definitions can complicate enterprise compliance strategies and require organisations to remain agile.

Enterprises subject to CARB must meet strict emissions disclosure rules set out under the Mandatory Reporting Regulation and the Climate Accountability Package. Under the related Financial Risk Act, companies must also submit climate risk reports that mandate the disclosure of climate-related financial risks and outline mitigation strategies to address these risks.

Effective sustainability management is required to capture accurate information, while transparent reporting ensures compliance, strengthens stakeholder trust, and supports alignment with California’s broader climate disclosure framework.

Which organisations need to report on CARB

CARB requires annual emissions reporting from facilities and suppliers that meet defined thresholds under the Mandatory Reporting Regulation (MRR). Under the latest CARB workshop, inclusion depends on revenue thresholds and whether the entity is doing business in California. This includes:

- Industrial facilities emitting more than 10,000 metric tonnes of CO₂e per year

- Electricity generators and importers

- Fuel suppliers, such as natural gas or petroleum providers

- Large companies with total annual revenues exceeding $1 billion (SB 253) or $500 million (SB 261) that do business in California

- Voluntary reporters who opt in to align with ESG commitments or investor expectations

CARB’s November 2025 workshop clarified that:

- Revenue is assessed using the lesser of the previous two fiscal years

- Gross receipts follow the definition under Revenue and Taxation Code § 25120

- Doing business in California aligns with Revenue and Taxation Code § 23101, excluding payroll and property tests

- Parent–subsidiary relationships do not determine regulation; each entity assesses its own obligations independently

- Non-profits and entities whose only presence in California is teleworking staff are exempt

What greenhouse gas emissions must be reported

CARB requires enterprises to provide a comprehensive and transparent emissions inventory that covers all material sources of greenhouse gas (GHG) emissions. Reporting must include all relevant carbon emissions and greenhouse gases as defined by CARB. This includes:

- Direct (Scope 1) emissions: Emissions from sources owned or controlled by the company, such as onsite fuel combustion, industrial processes, or company vehicles.

- Indirect (Scope 2) emissions: Emissions from the generation of purchased electricity, steam, heating, or cooling consumed by the organisation.

- Fuel use and process data: Detailed operational data used to calculate emissions accurately.

- Emissions factors and methodologies: The approved calculation methods and factors applied, which must follow CARB’s technical protocols.

- Electricity imports and exports: Data on purchased or distributed electricity, where applicable.

- Value chain (Scope 3) emissions: Indirect emissions across the wider supply chain, including supplier activity, business travel, and logistics that occur outside the company’s direct control.

By applying these protocols, enterprises ensure that direct and indirect emissions are accurately captured, with a focus on supply chain and travel-related impacts. Precision is critical, as estimates or incomplete data will not meet CARB’s requirements, and larger emitters are subject to third-party verification.

Updates from the November 2025 CARB workshop include:

- Scope 1 and Scope 2 reporting is required in 2026

- Scope 3 reporting will begin from 2027, with CARB currently gathering input on which of the 15 categories enterprises find most relevant

Precision is critical, as estimates or incomplete data will not meet CARB’s requirements, and larger emitters are subject to third-party verification.

Read our guide here for more information on Scope 1,2, and 3 emissions.

Reporting timelines and deadlines

Enterprises must follow a defined annual reporting cycle set by CARB, aligned with broader disclosure rules such as California’s SB 253 and SB 261:

- CARB now proposes a one-time first-year deadline of 10 August 2026 for SB 253 Scope 1 and Scope 2 reporting.

- Entities will report the fiscal year ending in 2025 or 2026 depending on their financial year-end, with at least six months allowed for preparation.

- Limited assurance is not required in 2026.

- Entities not collecting data at the time of the 2024 Enforcement Notice may submit a formal declaration instead of emissions data.

- SB 261 climate risk reports are due 1 January 2026 and must be posted on company websites and submitted to the CARB docket by 1 July 2026.

These deadlines allow very little flexibility. Incomplete or inconsistent data can delay verification or even lead to rejected submissions, exposing enterprises to regulatory and reputational risks.

The role of third-party verification

CARB confirmed in its November 2025 workshop that data assurance requirements for SB 253 will be set during a later rulemaking and do not apply to 2026 reporting.

Previously, CARB had detailed that third-party verification will be mandated to be conducted at various levels, including limited and reasonable assurance. Limited assurance involves verifying controls and processes, providing a lower level of confidence. In comparison, reasonable assurance requires a more in-depth audit, offering higher confidence in the reported data.

The verification process typically involves:

- Reviewing calculation methodologies and data sources

- Validating emissions factors and assumptions

- Assessing data management systems and supporting documentation

The company is responsible for establishing robust internal controls over its ESG data to support verification and ensure compliance with limited assurance or reasonable assurance standards. Strong governance ensures that records are consistent, transparent, and readily auditable.

Risks of CARB non-compliance

CARB has significant enforcement powers. Civil penalties may be imposed for non-compliance with climate disclosure regulations. Non-compliance exposes enterprises to significant risks that can impact their financial performance, shareholder value, and long-term resilience. Climate risks are heightened for directly affected companies that fail to comply.

Accurate and timely climate risk disclosures are essential to maintaining market confidence, protecting financial investments, and ensuring continuity of operations.

Financial penalties

Non-compliance can result in substantial fines, particularly for repeat offences. These penalties directly impact financial performance and may undermine investor confidence.

- Up to $500,000 per reporting year for violations under California’s Senate Bill 253 (e.g., late, missing, or inaccurate filings).

- Up to $37,500 per action under California Health & Safety Code § 43016, which CARB may apply to specific regulatory breaches.

- Penalties can also reach $10,000 per violation per day in certain enforcement cases, depending on severity and duration.

Reputational risk

Public disclosure of violations can damage brand credibility, weaken customer trust, and reduce employee morale. Reputational risk often carries longer-term consequences than financial penalties.

Operational limitations

CARB may suspend permits or restrict business activities for serious violations. Such operational constraints can disrupt supply chains and create uncertainty for lenders and partners.

Why manual reporting methods create risk

Some enterprises continue to use spreadsheets or manual systems for emissions reporting. While inexpensive in the short term, these tools are unsuited to the scale and complexity of enterprise compliance.

They increase exposure to climate-related risks, limit transparency, and make it harder to align with regulatory requirements or demonstrate resilience to physical and transition risks.

In contrast, dedicated reporting systems provide robust governance, track energy consumption across supply chains, and support transparent disclosures that strengthen trust in the financial markets and safeguard long-term economic outcomes. Reliable data also ensures that sustainability management integrates effectively with broader corporate operations.

Error rates

Manual data entry is prone to mistakes, particularly when multiple stakeholders are involved in compiling emissions records. Inconsistent version control adds further risk, creating conflicting datasets that undermine reporting confidence. These inaccuracies complicate compliance, can create costly delays during verification, and damage credibility with regulators and investors.

Inefficiency

Collecting and validating emissions data manually requires significant time and effort, diverting resources from higher-value sustainability initiatives. Enterprises often face bottlenecks when consolidating data across multiple facilities or suppliers. This inefficiency slows compliance reporting and limits the ability to analyse trends, set reduction targets, and respond quickly to regulatory changes.

Lack of governance

Spreadsheets rarely provide the structured controls required for enterprise-grade compliance. Organisations struggle to demonstrate accountability without audit trails, version history, or defined approval workflows. This lack of governance exposes enterprises to regulatory scrutiny and weakens the assurance of ESG disclosures, leaving sustainability data vulnerable to challenges during audits and verification processes.

Best practices for CARB reporting

Adopting structured best practices is essential for reducing compliance risk and improving efficiency. CARB continues to provide regular workshops and updated FAQs to help enterprises understand their obligations.

Updates include:

- ensuring alignment with the latest SB 253 Scope 1–2 draft template, although use of the template is optional for 2026

- preparing for future rulemakings covering data assurance, recurring deadlines and Scope 3 templates

Strengthen data collection processes

Enterprises should implement robust systems for capturing and validating emissions information across facilities and supply chains. Accurate tracking of direct emissions and supporting data ensures that disclosures are regulator-ready. Strong internal controls reduce error rates and create the transparency needed for effective compliance.

Maintain governance and accountability

Review and update reporting procedures regularly to reflect the evolving CARB rules and global standards, such as the TCFD and the Greenhouse Gas Protocol. Structured sign-off processes and audit trails help preserve accountability, reinforcing the credibility of climate disclosures with regulators, investors, and internal stakeholders.

Build staff capability

Training teams responsible for sustainability reporting is critical. Skilled staff ensure consistent methodologies and accurate reporting, reducing non-compliance risk. Embedding best practice knowledge across departments helps align emissions data with broader ESG strategy.

Leverage technology solutions

Dedicated ESG software like KEY ESG streamlines reporting workflows, consolidates data across business units, and minimises errors. Automated systems improve efficiency and provide audit-ready outputs, enabling enterprises to adapt quickly to changes in legislation such as California's Climate Corporate Data Accountability Act (SB 253).

Align with financial and strategic priorities

CARB compliance is not only about regulation; it also supports market positioning. Aligning with CARB requirements helps companies advance their net-zero emissions goals by integrating climate action into their broader sustainability strategies. Transparent disclosures strengthen stakeholder trust, protect financial standing, and meet the expectations of institutional investments seeking credible ESG performance.

These practices prepare enterprises for broader sustainability requirements under the California Climate Disclosure Laws and the EU CSRD.

Fulfill CARB reporting requirements with KEY ESG

CARB reporting is complex, with strict thresholds, timelines, and evolving templates, definitions and future assurance requirements. For enterprises, success depends on accurate data, robust governance, and transparent climate risk disclosures that protect compliance and strengthen stakeholder confidence. Spreadsheets and manual methods cannot deliver the reliability or efficiency needed at scale.

KEY ESG's carbon accounting platform provides the structure enterprises need to meet these demands. With real-time reporting, built-in data validation, and audit-ready outputs, organisations can confidently manage CARB compliance while aligning with broader ESG and climate disclosure regulations.

Request a demo today to see how KEY ESG helps enterprises simplify compliance and gain better control over their CARB reporting requirements.

California is at the forefront of climate regulation in the US, and one of the most important agencies driving this progress is the California Air Resources Board (CARB). The state’s climate disclosure laws, shaped by Senate Bill 253 and Senate Bill 261, together with Senate Bill 219, form the foundation of California’s approach to corporate climate accountability.

CARB’s greenhouse gas (GHG) reporting rules are detailed and mandatory for any large enterprise operating in or doing business with California. These requirements are part of California’s broader Climate Accountability Package, which aims to increase transparency and expand corporate disclosure obligations.

Failing to comply can result in penalties, reputational harm, and delays in achieving ESG goals. Companies are also under growing pressure to improve voluntary carbon market disclosures and align with international standards such as the Corporate Sustainability Reporting Directive (CSRD).

This guide outlines CARB’s reporting requirements, including who must comply, what data to report, and the key risks associated with non-compliance.

What is the California Air Resources Board (CARB)?

The California Air Resources Board (CARB) is the state agency tasked with protecting public health by reducing air pollution and addressing climate change. Established in 1967, it remains one of the world’s most progressive and influential environmental regulators.

CARB develops and enforces rules that target greenhouse gas emissions, air quality, and the adoption of clean technology. In addition, this agency issues draft regulations for public comment, and these drafts are shaped by input from frameworks such as the Task Force on Climate-Related Financial Disclosures (TCFD).

Its frameworks, including California’s reporting requirements, are specifically designed to support the state’s ambitious climate objectives, including achieving carbon neutrality by 2045.

Why CARB matters for climate disclosure laws

For enterprises, CARB requirements are more than a compliance exercise. They set the standard for how emissions should be measured and reported. California's climate disclosure laws, including SB 253, SB 261 and SB 219, are among the nation's most comprehensive and are often compared to other frameworks like the SEC's climate disclosure rules. The development of these laws involves significant public input, including public workshops hosted by regulatory agencies, which allow stakeholders to provide feedback and help shape the final regulations.

As California is a global leader in climate regulation, CARB’s frameworks are often mirrored by other states and countries. As a result, enterprises must navigate varying regulatory requirements and face significant compliance burdens as they adapt to different reporting standards across jurisdictions.

This means that compliance with CARB ensures access to the California market and prepares enterprises for broader regulatory shifts worldwide. However, ongoing regulatory uncertainty and frequent updates to programme rules, templates and definitions can complicate enterprise compliance strategies and require organisations to remain agile.

Enterprises subject to CARB must meet strict emissions disclosure rules set out under the Mandatory Reporting Regulation and the Climate Accountability Package. Under the related Financial Risk Act, companies must also submit climate risk reports that mandate the disclosure of climate-related financial risks and outline mitigation strategies to address these risks.

Effective sustainability management is required to capture accurate information, while transparent reporting ensures compliance, strengthens stakeholder trust, and supports alignment with California’s broader climate disclosure framework.

Which organisations need to report on CARB

CARB requires annual emissions reporting from facilities and suppliers that meet defined thresholds under the Mandatory Reporting Regulation (MRR). Under the latest CARB workshop, inclusion depends on revenue thresholds and whether the entity is doing business in California. This includes:

- Industrial facilities emitting more than 10,000 metric tonnes of CO₂e per year

- Electricity generators and importers

- Fuel suppliers, such as natural gas or petroleum providers

- Large companies with total annual revenues exceeding $1 billion (SB 253) or $500 million (SB 261) that do business in California

- Voluntary reporters who opt in to align with ESG commitments or investor expectations

CARB’s November 2025 workshop clarified that:

- Revenue is assessed using the lesser of the previous two fiscal years

- Gross receipts follow the definition under Revenue and Taxation Code § 25120

- Doing business in California aligns with Revenue and Taxation Code § 23101, excluding payroll and property tests

- Parent–subsidiary relationships do not determine regulation; each entity assesses its own obligations independently

- Non-profits and entities whose only presence in California is teleworking staff are exempt

What greenhouse gas emissions must be reported

CARB requires enterprises to provide a comprehensive and transparent emissions inventory that covers all material sources of greenhouse gas (GHG) emissions. Reporting must include all relevant carbon emissions and greenhouse gases as defined by CARB. This includes:

- Direct (Scope 1) emissions: Emissions from sources owned or controlled by the company, such as onsite fuel combustion, industrial processes, or company vehicles.

- Indirect (Scope 2) emissions: Emissions from the generation of purchased electricity, steam, heating, or cooling consumed by the organisation.

- Fuel use and process data: Detailed operational data used to calculate emissions accurately.

- Emissions factors and methodologies: The approved calculation methods and factors applied, which must follow CARB’s technical protocols.

- Electricity imports and exports: Data on purchased or distributed electricity, where applicable.

- Value chain (Scope 3) emissions: Indirect emissions across the wider supply chain, including supplier activity, business travel, and logistics that occur outside the company’s direct control.

By applying these protocols, enterprises ensure that direct and indirect emissions are accurately captured, with a focus on supply chain and travel-related impacts. Precision is critical, as estimates or incomplete data will not meet CARB’s requirements, and larger emitters are subject to third-party verification.

Updates from the November 2025 CARB workshop include:

- Scope 1 and Scope 2 reporting is required in 2026

- Scope 3 reporting will begin from 2027, with CARB currently gathering input on which of the 15 categories enterprises find most relevant

Precision is critical, as estimates or incomplete data will not meet CARB’s requirements, and larger emitters are subject to third-party verification.

Read our guide here for more information on Scope 1,2, and 3 emissions.

Reporting timelines and deadlines

Enterprises must follow a defined annual reporting cycle set by CARB, aligned with broader disclosure rules such as California’s SB 253 and SB 261:

- CARB now proposes a one-time first-year deadline of 10 August 2026 for SB 253 Scope 1 and Scope 2 reporting.

- Entities will report the fiscal year ending in 2025 or 2026 depending on their financial year-end, with at least six months allowed for preparation.

- Limited assurance is not required in 2026.

- Entities not collecting data at the time of the 2024 Enforcement Notice may submit a formal declaration instead of emissions data.

- SB 261 climate risk reports are due 1 January 2026 and must be posted on company websites and submitted to the CARB docket by 1 July 2026.

These deadlines allow very little flexibility. Incomplete or inconsistent data can delay verification or even lead to rejected submissions, exposing enterprises to regulatory and reputational risks.

The role of third-party verification

CARB confirmed in its November 2025 workshop that data assurance requirements for SB 253 will be set during a later rulemaking and do not apply to 2026 reporting.

Previously, CARB had detailed that third-party verification will be mandated to be conducted at various levels, including limited and reasonable assurance. Limited assurance involves verifying controls and processes, providing a lower level of confidence. In comparison, reasonable assurance requires a more in-depth audit, offering higher confidence in the reported data.

The verification process typically involves:

- Reviewing calculation methodologies and data sources

- Validating emissions factors and assumptions

- Assessing data management systems and supporting documentation

The company is responsible for establishing robust internal controls over its ESG data to support verification and ensure compliance with limited assurance or reasonable assurance standards. Strong governance ensures that records are consistent, transparent, and readily auditable.

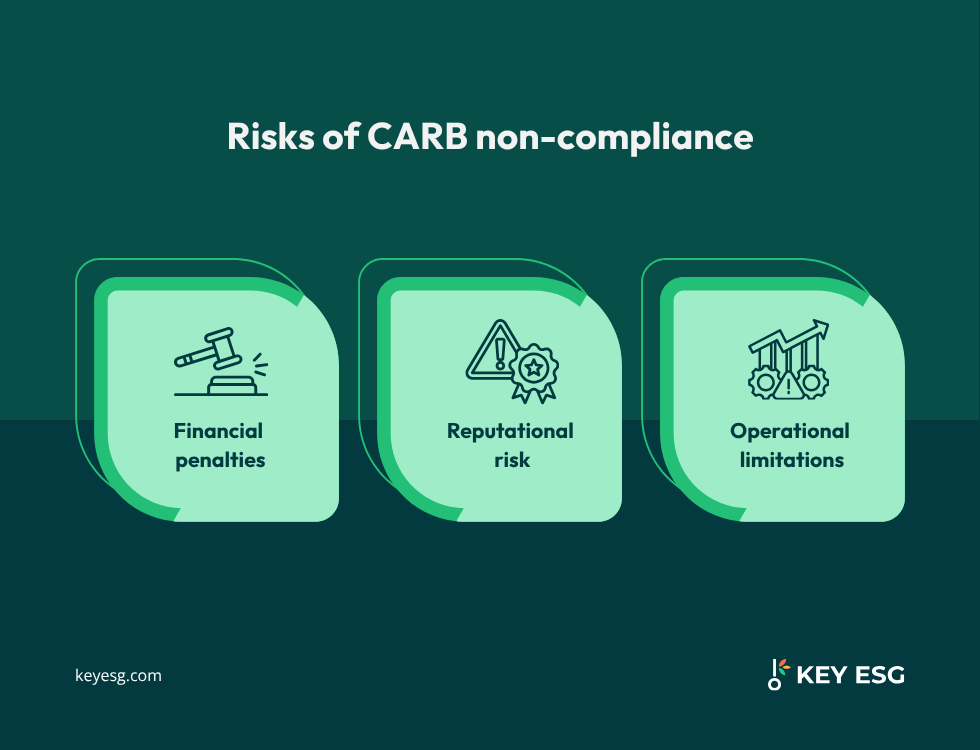

Risks of CARB non-compliance

CARB has significant enforcement powers. Civil penalties may be imposed for non-compliance with climate disclosure regulations. Non-compliance exposes enterprises to significant risks that can impact their financial performance, shareholder value, and long-term resilience. Climate risks are heightened for directly affected companies that fail to comply.

Accurate and timely climate risk disclosures are essential to maintaining market confidence, protecting financial investments, and ensuring continuity of operations.

Financial penalties

Non-compliance can result in substantial fines, particularly for repeat offences. These penalties directly impact financial performance and may undermine investor confidence.

- Up to $500,000 per reporting year for violations under California’s Senate Bill 253 (e.g., late, missing, or inaccurate filings).

- Up to $37,500 per action under California Health & Safety Code § 43016, which CARB may apply to specific regulatory breaches.

- Penalties can also reach $10,000 per violation per day in certain enforcement cases, depending on severity and duration.

Reputational risk

Public disclosure of violations can damage brand credibility, weaken customer trust, and reduce employee morale. Reputational risk often carries longer-term consequences than financial penalties.

Operational limitations

CARB may suspend permits or restrict business activities for serious violations. Such operational constraints can disrupt supply chains and create uncertainty for lenders and partners.

Why manual reporting methods create risk

Some enterprises continue to use spreadsheets or manual systems for emissions reporting. While inexpensive in the short term, these tools are unsuited to the scale and complexity of enterprise compliance.

They increase exposure to climate-related risks, limit transparency, and make it harder to align with regulatory requirements or demonstrate resilience to physical and transition risks.

In contrast, dedicated reporting systems provide robust governance, track energy consumption across supply chains, and support transparent disclosures that strengthen trust in the financial markets and safeguard long-term economic outcomes. Reliable data also ensures that sustainability management integrates effectively with broader corporate operations.

Error rates

Manual data entry is prone to mistakes, particularly when multiple stakeholders are involved in compiling emissions records. Inconsistent version control adds further risk, creating conflicting datasets that undermine reporting confidence. These inaccuracies complicate compliance, can create costly delays during verification, and damage credibility with regulators and investors.

Inefficiency

Collecting and validating emissions data manually requires significant time and effort, diverting resources from higher-value sustainability initiatives. Enterprises often face bottlenecks when consolidating data across multiple facilities or suppliers. This inefficiency slows compliance reporting and limits the ability to analyse trends, set reduction targets, and respond quickly to regulatory changes.

Lack of governance

Spreadsheets rarely provide the structured controls required for enterprise-grade compliance. Organisations struggle to demonstrate accountability without audit trails, version history, or defined approval workflows. This lack of governance exposes enterprises to regulatory scrutiny and weakens the assurance of ESG disclosures, leaving sustainability data vulnerable to challenges during audits and verification processes.

Best practices for CARB reporting

Adopting structured best practices is essential for reducing compliance risk and improving efficiency. CARB continues to provide regular workshops and updated FAQs to help enterprises understand their obligations.

Updates include:

- ensuring alignment with the latest SB 253 Scope 1–2 draft template, although use of the template is optional for 2026

- preparing for future rulemakings covering data assurance, recurring deadlines and Scope 3 templates

Strengthen data collection processes

Enterprises should implement robust systems for capturing and validating emissions information across facilities and supply chains. Accurate tracking of direct emissions and supporting data ensures that disclosures are regulator-ready. Strong internal controls reduce error rates and create the transparency needed for effective compliance.

Maintain governance and accountability

Review and update reporting procedures regularly to reflect the evolving CARB rules and global standards, such as the TCFD and the Greenhouse Gas Protocol. Structured sign-off processes and audit trails help preserve accountability, reinforcing the credibility of climate disclosures with regulators, investors, and internal stakeholders.

Build staff capability

Training teams responsible for sustainability reporting is critical. Skilled staff ensure consistent methodologies and accurate reporting, reducing non-compliance risk. Embedding best practice knowledge across departments helps align emissions data with broader ESG strategy.

Leverage technology solutions

Dedicated ESG software like KEY ESG streamlines reporting workflows, consolidates data across business units, and minimises errors. Automated systems improve efficiency and provide audit-ready outputs, enabling enterprises to adapt quickly to changes in legislation such as California's Climate Corporate Data Accountability Act (SB 253).

Align with financial and strategic priorities

CARB compliance is not only about regulation; it also supports market positioning. Aligning with CARB requirements helps companies advance their net-zero emissions goals by integrating climate action into their broader sustainability strategies. Transparent disclosures strengthen stakeholder trust, protect financial standing, and meet the expectations of institutional investments seeking credible ESG performance.

These practices prepare enterprises for broader sustainability requirements under the California Climate Disclosure Laws and the EU CSRD.

Fulfill CARB reporting requirements with KEY ESG

CARB reporting is complex, with strict thresholds, timelines, and evolving templates, definitions and future assurance requirements. For enterprises, success depends on accurate data, robust governance, and transparent climate risk disclosures that protect compliance and strengthen stakeholder confidence. Spreadsheets and manual methods cannot deliver the reliability or efficiency needed at scale.

KEY ESG's carbon accounting platform provides the structure enterprises need to meet these demands. With real-time reporting, built-in data validation, and audit-ready outputs, organisations can confidently manage CARB compliance while aligning with broader ESG and climate disclosure regulations.

Request a demo today to see how KEY ESG helps enterprises simplify compliance and gain better control over their CARB reporting requirements.

.png)

.avif)