For many organisations, Scope 3 emissions are the largest share of their carbon footprint, often originating across supply chains, transportation networks, and product lifecycles.

Scope 3 carbon accounting is also becoming more important for regulatory reporting and investor transparency. Frameworks such as CSRD and IFRS sustainability disclosure standards increasingly require organisations to report value-chain emissions where material.

Understanding how Scope 3 emissions are measured, the tools used to manage them, and the data challenges involved is now essential for enterprises aiming to track and reduce emissions.

Why Scope 3 emissions dominate corporate carbon footprints

For many organisations, most carbon emissions occur outside direct operations. While Scope 1 and Scope 2 emissions relate to fuel use and purchased energy, Scope 3 emissions arise across the broader value chain, including suppliers, logistics providers, product distribution, and product use.

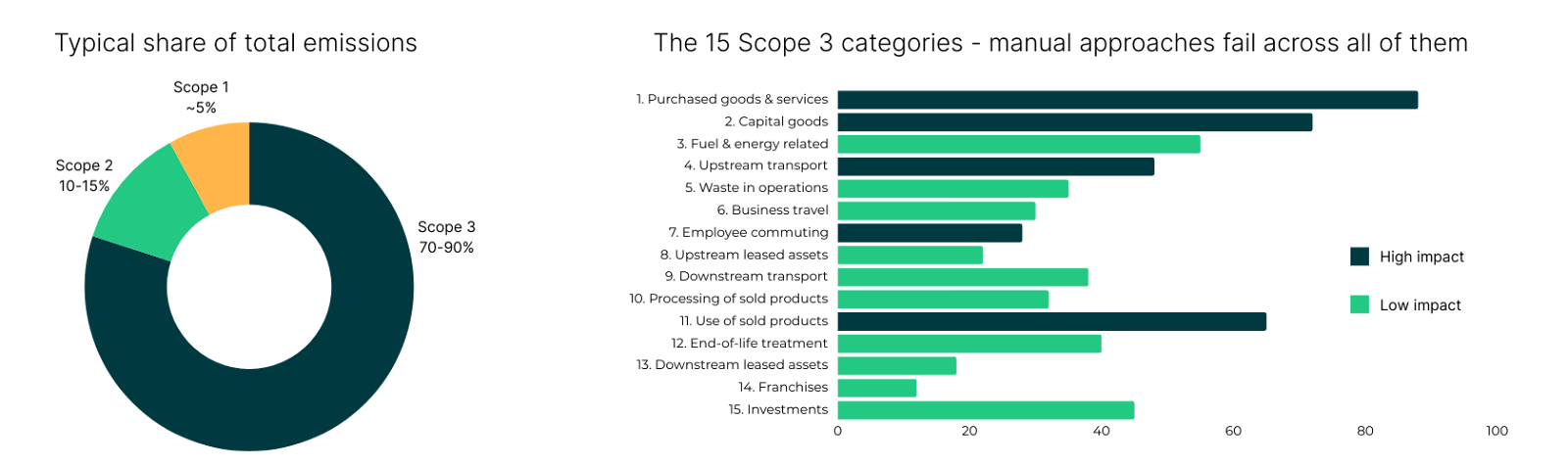

Studies across multiple industries suggest that Scope 3 emissions can account for 70–90 percent of a company’s total carbon footprint. This is particularly true for businesses that rely on complex supply chains or sell products with significant lifecycle impacts.

For example:

- Manufacturers may see large emissions linked to purchased materials and component suppliers.

- Retail and consumer goods companies frequently face emissions from transportation, distribution, and product use.

- Technology companies can experience significant emissions from hardware production and data centre supply chains.

- Financial institutions and investors may report emissions linked to financed activities or portfolio companies.

This value chain dependency is what makes Scope 3 carbon accounting significantly more complex than measuring operational emissions. Organisations must collect data from suppliers, procurement systems, logistics partners, and other external sources to build a complete picture of their greenhouse gas emissions.

What are the 15 Scope 3 emissions categories?

The Greenhouse Gas Protocol (GHG) defines fifteen Scope 3 categories that help organisations classify emissions across their value chains. These categories group indirect emissions that occur both upstream (before a product or service reaches the organisation) and downstream (after it leaves the organisation).

Understanding these categories helps enterprises identify where emissions occur and determine which parts of the value chain require data collection and measurement.

Upstream emissions

Upstream Scope 3 emissions relate to activities connected to suppliers, procurement, and operational inputs. These emissions frequently represent a large share of corporate carbon footprints because they capture the impact of purchased goods and services.

Key upstream categories include:

- Purchased goods and services

- Capital goods

- Fuel and energy-related activities not included in Scope 1 or 2

- Upstream transportation and distribution

- Waste generated in operations

- Business travel

- Employee commuting

- Upstream leased assets

Downstream emissions

Downstream emissions occur after products or services leave the organisation. These categories are particularly relevant for companies whose products generate emissions during use or disposal.

Key downstream categories include:

- Downstream transportation and distribution

- Processing of sold products

- Use of sold products

- End-of-life treatment of sold products

- Downstream leased assets

- Franchises

- Investments

Not every category is relevant for every organisation. Identifying which Scope 3 categories are material is a key step in building an effective carbon accounting approach.

Why is Scope 3 carbon accounting difficult for enterprises?

Measuring Scope 3 emissions is significantly more complex than calculating operational emissions. While Scope 1 and Scope 2 emissions are typically based on internal data such as fuel consumption and electricity use, Scope 3 emissions depend on information from across the value chain.

For enterprises and investment firms, this introduces several practical challenges.

Supply chain data gaps

Many organisations depend on suppliers to provide emissions data for purchased goods, services, and transportation activities. However, suppliers may lack the systems or resources required to calculate their own emissions.

As a result, companies frequently rely on spend-based estimates or industry emission factors, which can reduce the accuracy of Scope 3 calculations.

Fragmented operational data

Scope 3 emissions data often sits across multiple systems within an organisation. Procurement systems may contain supplier and purchasing data, logistics platforms hold transport information, and finance systems manage spending records.

Without structured integration across these sources, collecting consistent emissions data can become time-consuming and difficult to maintain.

Estimation versus primary data

Many organisations begin Scope 3 accounting using estimated emissions factors based on spending or industry averages. Over time, companies attempt to replace these estimates with supplier-specific emissions data.

Moving from estimated data to primary supplier data is one of the most challenging stages of Scope 3 carbon accounting.

Portfolio and multi-entity reporting

For investment firms and organisations managing multiple subsidiaries, Scope 3 accounting must also be performed across multiple entities or portfolio companies. Collecting consistent sustainability data across these structures requires coordinated reporting processes and standardised methodologies.

Audit readiness and regulatory expectations

Regulatory frameworks and investor expectations increasingly require organisations to provide transparent and traceable emissions data. This means Scope 3 calculations must be supported by documented methodologies, clear data sources, and evidence records that can support assurance processes.

For many enterprises, the difficulty of Scope 3 carbon accounting lies less in the calculation itself and more in establishing reliable data collection and governance processes across the value chain.

The compliance and reporting pressures

Regulatory frameworks and investor expectations are increasing the importance of reliable Scope 3 carbon accounting. Organisations are now expected to disclose value-chain emissions alongside operational emissions as part of broader sustainability reporting.

Several major sustainability disclosure frameworks now require organisations to report Scope 3 emissions where these are material:

- The Corporate Sustainability Reporting Directive (CSRD) requires many companies operating in the European Union to disclose value-chain emissions and document the methodologies used for emissions calculations.

- The IFRS Sustainability Disclosure Standards (IFRS S1 and S2) require companies to disclose climate-related risks, emissions data, and value-chain impacts where they are relevant to financial performance.

- The Sustainable Finance Disclosure Regulation (SFDR) requires financial market participants to report principal adverse impacts, including value chain emissions, where relevant to investments

- The California Climate Act requires large companies doing business in California to disclose Scope 1, Scope 2, and Scope 3 emissions, alongside climate-related financial risk

- The Science-Based Targets initiative (SBTi) requires companies setting science-based climate targets to measure and report Scope 3 emissions when they represent a significant share of total emissions.

These requirements increase the need for traceable emissions calculations, consistent methodologies, and structured sustainability data management.

Without reliable systems for collecting supplier data and documenting calculation methods, maintaining accurate Scope 3 disclosures can become increasingly difficult as reporting requirements expand.

Where most organisations start with Scope 3

Most organisations don’t begin Scope 3 accounting with full supplier data. Instead, they gradually improve data quality as sustainability reporting processes mature.

Common starting approaches include:

- Spend-based estimates, using procurement data and emission factor databases

- Activity-based calculations, using transport, logistics, or energy activity data

- Supplier-specific emissions data, collected directly from key suppliers as reporting programmes mature

Over time, organisations aim to increase the share of primary supplier emissions data used in Scope 3 reporting.

Tools used for Scope 3 carbon accounting

Managing Scope 3 emissions requires more than a single calculation tool. Because these emissions span the value chain, organisations typically rely on multiple systems to collect activity data, calculate emissions, and coordinate supplier engagement.

Enterprise sustainability teams frequently combine operational data sources with specialised carbon accounting platforms to build a structured Scope 3 reporting process.

Carbon accounting platforms

Carbon accounting platforms are used to calculate emissions across Scope 1, 2, and 3 using activity data and recognised emission factors. These systems apply methodologies aligned with the GHG Protocol and help organisations generate structured emissions inventories.

Platforms such as KEY ESG support Scope 3 accounting by mapping operational and supplier data to the relevant Scope 3 categories, applying emission factors from recognised databases, and maintaining audit-ready records for sustainability reporting.

Supplier engagement tools

Because many Scope 3 emissions originate from purchased goods and services, organisations frequently need to collect emissions data directly from suppliers.

Supplier engagement tools help companies request emissions information, distribute sustainability questionnaires, and standardise reporting formats across supply chains.

Procurement and ERP integrations

Many Scope 3 calculations rely on operational data from procurement and finance systems. Integration with ERP and procurement platforms allows sustainability teams to access purchasing data, supplier records, and logistics activity required for emissions calculations.

These integrations help reduce manual data collection and improve the consistency of Scope 3 reporting.

Emission factor databases

Emission factors are required to convert operational activity data into emissions estimates. Many carbon accounting systems rely on established databases such as DEFRA, the US EPA, and Climatiq, which provide thousands of emission factors covering materials, transport modes, and industry activities.

These databases allow organisations to estimate emissions when supplier-specific data is not yet available

KEY ESG brings Scope 3 carbon accounting into enterprise sustainability systems

Scope 3 carbon accounting requires organisations to measure emissions across complex value chains, coordinate data from multiple systems, and maintain consistent reporting methodologies. For many enterprises, managing these processes through spreadsheets or disconnected tools quickly becomes difficult as reporting requirements expand.

Enterprise sustainability platforms help centralise these processes by collecting operational and supplier data, applying recognised emissions methodologies, and maintaining structured records for sustainability reporting.

KEY ESG is designed to support this approach.

The platform enables organisations and investment firms to collect sustainability data across entities and portfolio companies, manage Scope 1, 2, and 3 carbon accounting, and align reporting with frameworks including CSRD, IFRS S1/S2, SFDR, TCFD and California Climate Laws.

It also supports AI-assisted workflows, including data validation and structured narrative reporting, helping teams manage both quantitative emissions data and qualitative disclosures required under frameworks such as CSRD.

By managing carbon accounting and sustainability reporting within a single system, organisations can improve data consistency, support audit-ready disclosures, and maintain clearer oversight of their sustainability performance.

Book a demo to see how KEY ESG brings all components of Scope 3 carbon accounting into a single unified platform.

For many organisations, Scope 3 emissions are the largest share of their carbon footprint, often originating across supply chains, transportation networks, and product lifecycles.

Scope 3 carbon accounting is also becoming more important for regulatory reporting and investor transparency. Frameworks such as CSRD and IFRS sustainability disclosure standards increasingly require organisations to report value-chain emissions where material.

Understanding how Scope 3 emissions are measured, the tools used to manage them, and the data challenges involved is now essential for enterprises aiming to track and reduce emissions.

Why Scope 3 emissions dominate corporate carbon footprints

For many organisations, most carbon emissions occur outside direct operations. While Scope 1 and Scope 2 emissions relate to fuel use and purchased energy, Scope 3 emissions arise across the broader value chain, including suppliers, logistics providers, product distribution, and product use.

Studies across multiple industries suggest that Scope 3 emissions can account for 70–90 percent of a company’s total carbon footprint. This is particularly true for businesses that rely on complex supply chains or sell products with significant lifecycle impacts.

For example:

- Manufacturers may see large emissions linked to purchased materials and component suppliers.

- Retail and consumer goods companies frequently face emissions from transportation, distribution, and product use.

- Technology companies can experience significant emissions from hardware production and data centre supply chains.

- Financial institutions and investors may report emissions linked to financed activities or portfolio companies.

This value chain dependency is what makes Scope 3 carbon accounting significantly more complex than measuring operational emissions. Organisations must collect data from suppliers, procurement systems, logistics partners, and other external sources to build a complete picture of their greenhouse gas emissions.

What are the 15 Scope 3 emissions categories?

The Greenhouse Gas Protocol (GHG) defines fifteen Scope 3 categories that help organisations classify emissions across their value chains. These categories group indirect emissions that occur both upstream (before a product or service reaches the organisation) and downstream (after it leaves the organisation).

Understanding these categories helps enterprises identify where emissions occur and determine which parts of the value chain require data collection and measurement.

Upstream emissions

Upstream Scope 3 emissions relate to activities connected to suppliers, procurement, and operational inputs. These emissions frequently represent a large share of corporate carbon footprints because they capture the impact of purchased goods and services.

Key upstream categories include:

- Purchased goods and services

- Capital goods

- Fuel and energy-related activities not included in Scope 1 or 2

- Upstream transportation and distribution

- Waste generated in operations

- Business travel

- Employee commuting

- Upstream leased assets

Downstream emissions

Downstream emissions occur after products or services leave the organisation. These categories are particularly relevant for companies whose products generate emissions during use or disposal.

Key downstream categories include:

- Downstream transportation and distribution

- Processing of sold products

- Use of sold products

- End-of-life treatment of sold products

- Downstream leased assets

- Franchises

- Investments

Not every category is relevant for every organisation. Identifying which Scope 3 categories are material is a key step in building an effective carbon accounting approach.

Why is Scope 3 carbon accounting difficult for enterprises?

Measuring Scope 3 emissions is significantly more complex than calculating operational emissions. While Scope 1 and Scope 2 emissions are typically based on internal data such as fuel consumption and electricity use, Scope 3 emissions depend on information from across the value chain.

For enterprises and investment firms, this introduces several practical challenges.

Supply chain data gaps

Many organisations depend on suppliers to provide emissions data for purchased goods, services, and transportation activities. However, suppliers may lack the systems or resources required to calculate their own emissions.

As a result, companies frequently rely on spend-based estimates or industry emission factors, which can reduce the accuracy of Scope 3 calculations.

Fragmented operational data

Scope 3 emissions data often sits across multiple systems within an organisation. Procurement systems may contain supplier and purchasing data, logistics platforms hold transport information, and finance systems manage spending records.

Without structured integration across these sources, collecting consistent emissions data can become time-consuming and difficult to maintain.

Estimation versus primary data

Many organisations begin Scope 3 accounting using estimated emissions factors based on spending or industry averages. Over time, companies attempt to replace these estimates with supplier-specific emissions data.

Moving from estimated data to primary supplier data is one of the most challenging stages of Scope 3 carbon accounting.

Portfolio and multi-entity reporting

For investment firms and organisations managing multiple subsidiaries, Scope 3 accounting must also be performed across multiple entities or portfolio companies. Collecting consistent sustainability data across these structures requires coordinated reporting processes and standardised methodologies.

Audit readiness and regulatory expectations

Regulatory frameworks and investor expectations increasingly require organisations to provide transparent and traceable emissions data. This means Scope 3 calculations must be supported by documented methodologies, clear data sources, and evidence records that can support assurance processes.

For many enterprises, the difficulty of Scope 3 carbon accounting lies less in the calculation itself and more in establishing reliable data collection and governance processes across the value chain.

The compliance and reporting pressures

Regulatory frameworks and investor expectations are increasing the importance of reliable Scope 3 carbon accounting. Organisations are now expected to disclose value-chain emissions alongside operational emissions as part of broader sustainability reporting.

Several major sustainability disclosure frameworks now require organisations to report Scope 3 emissions where these are material:

- The Corporate Sustainability Reporting Directive (CSRD) requires many companies operating in the European Union to disclose value-chain emissions and document the methodologies used for emissions calculations.

- The IFRS Sustainability Disclosure Standards (IFRS S1 and S2) require companies to disclose climate-related risks, emissions data, and value-chain impacts where they are relevant to financial performance.

- The Sustainable Finance Disclosure Regulation (SFDR) requires financial market participants to report principal adverse impacts, including value chain emissions, where relevant to investments

- The California Climate Act requires large companies doing business in California to disclose Scope 1, Scope 2, and Scope 3 emissions, alongside climate-related financial risk

- The Science-Based Targets initiative (SBTi) requires companies setting science-based climate targets to measure and report Scope 3 emissions when they represent a significant share of total emissions.

These requirements increase the need for traceable emissions calculations, consistent methodologies, and structured sustainability data management.

Without reliable systems for collecting supplier data and documenting calculation methods, maintaining accurate Scope 3 disclosures can become increasingly difficult as reporting requirements expand.

Where most organisations start with Scope 3

Most organisations don’t begin Scope 3 accounting with full supplier data. Instead, they gradually improve data quality as sustainability reporting processes mature.

Common starting approaches include:

- Spend-based estimates, using procurement data and emission factor databases

- Activity-based calculations, using transport, logistics, or energy activity data

- Supplier-specific emissions data, collected directly from key suppliers as reporting programmes mature

Over time, organisations aim to increase the share of primary supplier emissions data used in Scope 3 reporting.

Tools used for Scope 3 carbon accounting

Managing Scope 3 emissions requires more than a single calculation tool. Because these emissions span the value chain, organisations typically rely on multiple systems to collect activity data, calculate emissions, and coordinate supplier engagement.

Enterprise sustainability teams frequently combine operational data sources with specialised carbon accounting platforms to build a structured Scope 3 reporting process.

Carbon accounting platforms

Carbon accounting platforms are used to calculate emissions across Scope 1, 2, and 3 using activity data and recognised emission factors. These systems apply methodologies aligned with the GHG Protocol and help organisations generate structured emissions inventories.

Platforms such as KEY ESG support Scope 3 accounting by mapping operational and supplier data to the relevant Scope 3 categories, applying emission factors from recognised databases, and maintaining audit-ready records for sustainability reporting.

Supplier engagement tools

Because many Scope 3 emissions originate from purchased goods and services, organisations frequently need to collect emissions data directly from suppliers.

Supplier engagement tools help companies request emissions information, distribute sustainability questionnaires, and standardise reporting formats across supply chains.

Procurement and ERP integrations

Many Scope 3 calculations rely on operational data from procurement and finance systems. Integration with ERP and procurement platforms allows sustainability teams to access purchasing data, supplier records, and logistics activity required for emissions calculations.

These integrations help reduce manual data collection and improve the consistency of Scope 3 reporting.

Emission factor databases

Emission factors are required to convert operational activity data into emissions estimates. Many carbon accounting systems rely on established databases such as DEFRA, the US EPA, and Climatiq, which provide thousands of emission factors covering materials, transport modes, and industry activities.

These databases allow organisations to estimate emissions when supplier-specific data is not yet available

KEY ESG brings Scope 3 carbon accounting into enterprise sustainability systems

Scope 3 carbon accounting requires organisations to measure emissions across complex value chains, coordinate data from multiple systems, and maintain consistent reporting methodologies. For many enterprises, managing these processes through spreadsheets or disconnected tools quickly becomes difficult as reporting requirements expand.

Enterprise sustainability platforms help centralise these processes by collecting operational and supplier data, applying recognised emissions methodologies, and maintaining structured records for sustainability reporting.

KEY ESG is designed to support this approach.

The platform enables organisations and investment firms to collect sustainability data across entities and portfolio companies, manage Scope 1, 2, and 3 carbon accounting, and align reporting with frameworks including CSRD, IFRS S1/S2, SFDR, TCFD and California Climate Laws.

It also supports AI-assisted workflows, including data validation and structured narrative reporting, helping teams manage both quantitative emissions data and qualitative disclosures required under frameworks such as CSRD.

By managing carbon accounting and sustainability reporting within a single system, organisations can improve data consistency, support audit-ready disclosures, and maintain clearer oversight of their sustainability performance.

Book a demo to see how KEY ESG brings all components of Scope 3 carbon accounting into a single unified platform.