Global ESG reporting is entering a new phase. Regulations are expanding, voluntary standards are maturing, and expectations for credible, decision-useful sustainability data are rising across consumers, investors and shareholders.

Organisations now face a mixture of mandatory rules, sector-specific requirements, and voluntary frameworks that increasingly shape capital flows and corporate behaviour. Understanding how these frameworks differ - and where they overlap - helps reporting teams plan efficiently, reduce duplication, and build audit-ready processes.

This article compares ten of the most influential ESG frameworks worldwide. It highlights what each one requires, who must comply, and what these developments mean for sustainability, compliance, and finance teams.

Why ESG reporting frameworks matter

Sustainability frameworks exist to make corporate information more consistent and comparable. They define what companies should disclose, how data should be measured, and which metrics matter to investors, regulators, and stakeholders.

Growing regulatory pressure has made ESG reporting a core requirement for organisations. European rules are prioritising granular, value-chain reporting. International standards are emphasising financial materiality and investor-focused metrics. New US state laws are bringing climate disclosures to a wider range of companies. Voluntary frameworks are continuing to influence market expectations, particularly in areas such as biodiversity and private equity.

Across regions, a general convergence is emerging: climate disclosures are becoming mandatory; scenario analysis and transition planning are becoming common; and value-chain data expectations are increasing. These trends underscore the need for clear systems and repeatable processes.

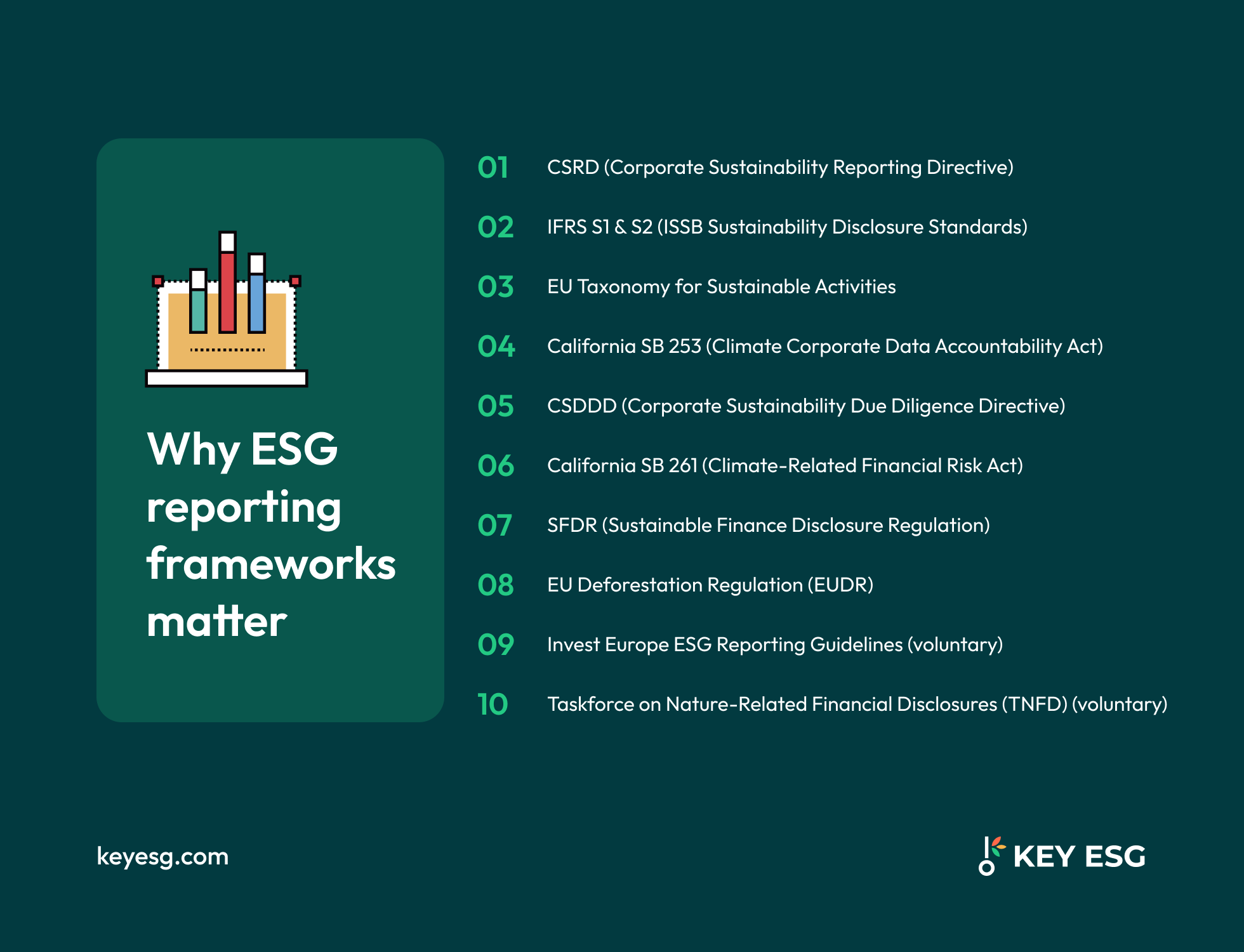

The top 10 global ESG reporting frameworks

1. CSRD (Corporate Sustainability Reporting Directive)

CSRD is the European Union’s most comprehensive sustainability disclosure regime and now covers thousands of companies both inside and outside the EU.

What CSRD requires

- Reporting using the European Sustainability Reporting Standards (ESRS).

- Double materiality assessments covering both financial impact and outward impacts.

- A wide set of data points covering climate, environment, workers, communities, business conduct, and governance.

- Value-chain data and clear documentation of methodologies.

- Mandatory limited assurance, evolving toward reasonable assurance.

Who must report

- Large EU companies with over 1,000 employees and a turnover of more than €50 million

- Listed SMEs (with phase-ins and opt-outs).

- Certain non-EU companies generating more than €450 million in revenue in the EU with significant EU subsidiaries or branches.

Why CSRD matters

CSRD sets one of the world’s most comprehensive ESG disclosure requirements. It integrates the EU Taxonomy, aligns in part with ISSB, and provides core data used by investors under frameworks such as SFDR. CSRD disclosures ensure that companies report financially material sustainability information, giving investors and stakeholders relevant, decision-useful insights for informed decision-making.

Challenges

Data availability, supplier engagement, and assurance readiness are common hurdles. Companies often need new systems to handle increased volume, ensure traceability, and maintain audit trails.

2. IFRS S1 & S2 (ISSB Sustainability Disclosure Standards)

The ISSB standards - IFRS S1 and S2 - developed by the International Sustainability Standards Board, provide a global baseline for sustainability and climate disclosures used by capital markets. These standards require organisations to use ESG metrics to measure and disclose their sustainability performance.

What the standards require

- IFRS S1: General sustainability disclosures covering governance, strategy, risk management, and metrics and targets.

- IFRS S2: Climate-related disclosures, aligned closely with TCFD, including Scope 1–3 emissions, transition plans, and scenario analysis.

Who uses ISSB

Countries adopting ISSB as a national baseline, multinational companies, and investors seeking consistent climate-risk information.

Why ISSB matters

ISSB aims to create sustainability information that is globally comparable. It focuses on financial materiality, making it highly relevant to CFOs, listed companies, and investors. It is also designed to interoperate with CSRD. For a detailed guide to IFRS S1 and S2, see our deep-dive explainer guide to the IFRS S1 and S2 metrics.

Australia’s adoption: AASB (ASRS)

Australia is adopting ISSB-aligned standards through the AASB Australian Sustainability Reporting Standards (ASRS).

Key points include:

- Reporting thresholds based on Australian size categories.

Mandatory phased implementation beginning with the largest companies. - Requirements that align with international guidance while incorporating the Australian context.

Challenges

Many organisations need to build capacity for scenario analysis, financial-impact modelling, and integration with financial reporting cycles.

3. EU Taxonomy for Sustainable Activities

The EU Taxonomy is a classification system defining which economic activities qualify as environmentally sustainable, guiding companies to disclose greenhouse gas emissions and address climate change. Our blog on the EU Taxonomy is a helpful guide for sustainability leaders looking for more detail on this reporting framework.

What it requires

- Assessment of activities against technical screening criteria for environmental objectives.

- Proof that activities “do no significant harm” and meet minimum social safeguards.

- Annual reporting of turnover, CapEx, and OpEx associated with Taxonomy-eligible and aligned activities.

Who must report

Large companies subject to the Corporate Sustainability Reporting Directive (CSRD) / Non-Financial Reporting Directive (NFRD), as well as certain financial-market participants and fund managers, are required to report the alignment of their activities or portfolios with the EU Taxonomy.

Why it matters

The Taxonomy influences investment decisions, lending strategies, and access to sustainable finance. It provides a framework for evaluating claims about green activities.

Challenges

Complex criteria, evolving delegated acts, and dependency on supplier data are common obstacles.

4. California SB 253 (Climate Corporate Data Accountability Act)

SB 253 introduces mandatory climate disclosure requirements for large companies operating in California, including many publicly traded companies that are already subject to climate disclosure regulations.

What it requires

- Annual public reporting of Scope 1, Scope 2, and Scope 3 emissions following the Greenhouse Gas Protocol.

- Third-party assurance is aligned with phased assurance levels.

Who must report

Companies with more than $1 billion in annual revenue doing business in California. This includes many global organisations headquartered outside the United States.

Why it matters

SB 253 is one of the first laws in the US to require full-value chain emissions reporting, including Scope 3.

Challenges

Scope 3 quantification, supplier engagement, data estimation methodologies, and assurance preparation.

5. CSDDD (Corporate Sustainability Due Diligence Directive)

CSDDD aims to improve human rights and environmental due diligence across global value chains by enhancing sustainability efforts and managing ESG risks throughout business operations.

What it requires

- Identification, prevention, mitigation, and remediation of adverse impacts.

- Integration of due diligence into policies and risk-management systems.

- Development of climate transition plans.

- Public reporting on due diligence processes and outcomes.

Who must comply

Large EU companies and non-EU companies with significant revenue and presence in the EU.

Why it matters

CSDDD shifts responsibility from disclosure to ongoing due diligence action. It intersects with CSRD because due diligence performance feeds into ESRS disclosures.

Challenges

Value-chain mapping, risk scoring, documentation, organisational oversight, and supplier engagement.

6. California SB 261 (Climate-Related Financial Risk Act)

SB 261 is designed to improve transparency around climate-related financial risks, particularly impacting the financial sector and aligning with global standards for climate-related financial disclosures.

What it requires

The law draws on recommendations from the Task Force on Climate-related Financial Disclosures (TCFD), a leading force on climate-related reporting, to guide organisations in assessing and disclosing climate risks and opportunities.

- Biennial climate-risk reports aligned with TCFD and ISSB guidance.

- Disclosures on governance, risk processes, strategy, and financial exposures to physical and transition risks.

Who must report

Companies with over $500 million in annual revenue doing business in California.

Why it matters

It brings climate-risk reporting into the mainstream for US-based and global companies.

Challenges

Scenario modelling, quantifying financial implications, and linking climate risks to enterprise risk management.

7. SFDR (Sustainable Finance Disclosure Regulation)

SFDR governs sustainability disclosures for financial market participants in the EU and is influenced by international standards set by organisations such as the Financial Stability Board.

What it requires

Firms must report on ESG factors and make ESG disclosures at both the entity and product levels.

- Entity- and product-level disclosures.

- Reporting of Principal Adverse Impact (PAI) indicators.

- Classification of funds as Article 6, 8, or 9 with specific reporting expectations.

Who must report

SFDR applies to EU-based asset managers, funds, and financial advisers, as well as certain non-EU managers marketing financial products in the EU.

Why it matters

SFDR shapes investment flows and is closely linked with both the EU Taxonomy and CSRD, creating a data dependency chain from corporates to financial institutions.

Challenges

Interpretation of PAI indicators, reliance on portfolio-company data, and adapting to regulatory updates.

8. EU Deforestation Regulation (EUDR)

EUDR aims to ensure that commodities placed on or exported from the EU market are deforestation-free.

What it requires

- Geolocation data for relevant commodities and products.

- Due diligence statements demonstrating compliance.

- Risk assessments and mitigation measures.

Who must report

Operators and traders dealing in covered commodities such as palm oil, soy, cattle, cocoa, coffee, rubber, and timber.

Why it matters

The regulation raises expectations for value-chain traceability and environmental due diligence.

Challenges

Collecting geolocation information, verifying supplier practices, and integrating traceability systems.

9. Invest Europe ESG Reporting Guidelines (voluntary)

The Invest Europe template is widely used in the private equity and venture capital sector as an example of voluntary ESG reporting frameworks.

What it provides

The guidelines help firms structure their ESG disclosures, support ESG initiatives, and facilitate ESG reporting within mainstream corporate reports, such as annual reports.

- Standardised ESG templates and KPIs for portfolio companies.

- Guidance for fund-level and firm-level reporting.

- Voluntary alignment with EU sustainability policies.

Who uses it

Private equity firms, venture funds, and LPs investing in European markets.

Why it matters

It improves interoperability between SFDR, EDCI and CSRD frameworks and provides a comparable baseline for ESG data in the European private markets. As a Supported Technology Vendor, KEY ESG enables seamless integration of the Invest Europe ESG template to streamline data collection and reporting.

Limitations

As a voluntary framework, it does not carry legal enforcement. However, it does reflect industry expectations.

10. Taskforce on Nature-Related Financial Disclosures (TNFD) (voluntary)

The TNFD is a task force focused on nature-related financial disclosures. TNFD provides a framework for assessing nature-related impacts, risks, and opportunities.

By addressing nature-related risks and opportunities, TNFD's work supports the transition to a sustainable future, helping organisations make informed decisions that benefit both society and the planet.

What it requires

- Application of the LEAP methodology: Locate, Evaluate, Assess, Prepare.

- Analysis of nature dependencies and impacts.

- Disclosure structure mirroring TCFD: governance, strategy, risk, metrics, and targets.

Who uses it

Companies and financial institutions are preparing for emerging nature-reporting regulations or investor expectations.

Why it matters

Nature-related risks - such as water scarcity, land degradation, and biodiversity loss - are rising on regulatory and investor agendas.

Challenges

Limited data availability, new metrics, and integration of nature factors into risk frameworks.

What do these frameworks mean for reporting teams?

The expansion of ESG regulations increases the need for coordinated workflows across sustainability, finance, procurement, and risk teams. Several themes are consistent across the ten frameworks:

- Wider value-chain expectations: CSRD, CSDDD, EUDR, SB 253, and SFDR all depend on high-quality supplier or portfolio-company data.

- Climate becoming mandatory: IFRS S2, AASB ASRS, SB 253, and SB 261 push climate disclosures into mainstream reporting.

- Scenario analysis and transition plans: These are now required or strongly recommended across multiple frameworks, increasing modelling and forecasting needs.

- Audit and assurance: CSRD, SB 253, and future ISSB implementations raise the bar for documentation, traceability, and controls.

- Interoperability challenges: Organisations must understand how one framework feeds another, for example, CSRD data supporting SFDR, or ISSB aligning with TCFD.

These developments make it essential to centralise data, standardise processes, and maintain reliable audit trails.

How KEY ESG helps organisations meet global reporting requirements

Growing regulatory complexity increases the need for integrated systems. As a leading ESG software, KEY ESG supports organisations across all major global reporting requirements.

Collect

- Centralised ESG and carbon data across departments and geographies.

- Support for GHG Protocol methodologies and 70,000+ emission factors from DEFRA, US EPA, and Climatiq.

- Supplier and value-chain data collection tools.

Comply

- Structured workflows aligned with CSRD/ESRS, ISSB/AASB, EU Taxonomy, SFDR, EUDR, SB 253, SB 261, and TNFD.

- Coverage of mandatory and voluntary frameworks with compliance support built in.

Report

- Automated disclosure outputs, audit-ready evidence logs, and version control.

- Templates aligned with key frameworks for faster reporting cycles.

Improve

- Insights into performance trends, risk exposure, and reduction opportunities.

- Support for transition planning and scenario modelling.

Carbon Accounting

- Full Scope 1–3 coverage aligned with the GHG Protocol.

- Transparent methodologies and automated audit-trails of emission factor calculation.

Moving forward with confidence in ESG reporting

ESG reporting is accelerating globally, driven by regulatory mandates, investor expectations, and market pressures.

As these frameworks continue to converge, having robust, scalable systems becomes essential. A robust sustainability strategy is crucial for long-term success in ESG reporting, helping organisations set clear goals, demonstrate accountability, and drive sustainable development.

Request a demo to see how KEY ESG streamlines ESG data collection, verification, and reporting - giving your organisation confidence across every global framework.

Global ESG reporting is entering a new phase. Regulations are expanding, voluntary standards are maturing, and expectations for credible, decision-useful sustainability data are rising across consumers, investors and shareholders.

Organisations now face a mixture of mandatory rules, sector-specific requirements, and voluntary frameworks that increasingly shape capital flows and corporate behaviour. Understanding how these frameworks differ - and where they overlap - helps reporting teams plan efficiently, reduce duplication, and build audit-ready processes.

This article compares ten of the most influential ESG frameworks worldwide. It highlights what each one requires, who must comply, and what these developments mean for sustainability, compliance, and finance teams.

Why ESG reporting frameworks matter

Sustainability frameworks exist to make corporate information more consistent and comparable. They define what companies should disclose, how data should be measured, and which metrics matter to investors, regulators, and stakeholders.

Growing regulatory pressure has made ESG reporting a core requirement for organisations. European rules are prioritising granular, value-chain reporting. International standards are emphasising financial materiality and investor-focused metrics. New US state laws are bringing climate disclosures to a wider range of companies. Voluntary frameworks are continuing to influence market expectations, particularly in areas such as biodiversity and private equity.

Across regions, a general convergence is emerging: climate disclosures are becoming mandatory; scenario analysis and transition planning are becoming common; and value-chain data expectations are increasing. These trends underscore the need for clear systems and repeatable processes.

The top 10 global ESG reporting frameworks

1. CSRD (Corporate Sustainability Reporting Directive)

CSRD is the European Union’s most comprehensive sustainability disclosure regime and now covers thousands of companies both inside and outside the EU.

What CSRD requires

- Reporting using the European Sustainability Reporting Standards (ESRS).

- Double materiality assessments covering both financial impact and outward impacts.

- A wide set of data points covering climate, environment, workers, communities, business conduct, and governance.

- Value-chain data and clear documentation of methodologies.

- Mandatory limited assurance, evolving toward reasonable assurance.

Who must report

- Large EU companies with over 1,000 employees and a turnover of more than €50 million

- Listed SMEs (with phase-ins and opt-outs).

- Certain non-EU companies generating more than €450 million in revenue in the EU with significant EU subsidiaries or branches.

Why CSRD matters

CSRD sets one of the world’s most comprehensive ESG disclosure requirements. It integrates the EU Taxonomy, aligns in part with ISSB, and provides core data used by investors under frameworks such as SFDR. CSRD disclosures ensure that companies report financially material sustainability information, giving investors and stakeholders relevant, decision-useful insights for informed decision-making.

Challenges

Data availability, supplier engagement, and assurance readiness are common hurdles. Companies often need new systems to handle increased volume, ensure traceability, and maintain audit trails.

2. IFRS S1 & S2 (ISSB Sustainability Disclosure Standards)

The ISSB standards - IFRS S1 and S2 - developed by the International Sustainability Standards Board, provide a global baseline for sustainability and climate disclosures used by capital markets. These standards require organisations to use ESG metrics to measure and disclose their sustainability performance.

What the standards require

- IFRS S1: General sustainability disclosures covering governance, strategy, risk management, and metrics and targets.

- IFRS S2: Climate-related disclosures, aligned closely with TCFD, including Scope 1–3 emissions, transition plans, and scenario analysis.

Who uses ISSB

Countries adopting ISSB as a national baseline, multinational companies, and investors seeking consistent climate-risk information.

Why ISSB matters

ISSB aims to create sustainability information that is globally comparable. It focuses on financial materiality, making it highly relevant to CFOs, listed companies, and investors. It is also designed to interoperate with CSRD. For a detailed guide to IFRS S1 and S2, see our deep-dive explainer guide to the IFRS S1 and S2 metrics.

Australia’s adoption: AASB (ASRS)

Australia is adopting ISSB-aligned standards through the AASB Australian Sustainability Reporting Standards (ASRS).

Key points include:

- Reporting thresholds based on Australian size categories.

Mandatory phased implementation beginning with the largest companies. - Requirements that align with international guidance while incorporating the Australian context.

Challenges

Many organisations need to build capacity for scenario analysis, financial-impact modelling, and integration with financial reporting cycles.

3. EU Taxonomy for Sustainable Activities

The EU Taxonomy is a classification system defining which economic activities qualify as environmentally sustainable, guiding companies to disclose greenhouse gas emissions and address climate change. Our blog on the EU Taxonomy is a helpful guide for sustainability leaders looking for more detail on this reporting framework.

What it requires

- Assessment of activities against technical screening criteria for environmental objectives.

- Proof that activities “do no significant harm” and meet minimum social safeguards.

- Annual reporting of turnover, CapEx, and OpEx associated with Taxonomy-eligible and aligned activities.

Who must report

Large companies subject to the Corporate Sustainability Reporting Directive (CSRD) / Non-Financial Reporting Directive (NFRD), as well as certain financial-market participants and fund managers, are required to report the alignment of their activities or portfolios with the EU Taxonomy.

Why it matters

The Taxonomy influences investment decisions, lending strategies, and access to sustainable finance. It provides a framework for evaluating claims about green activities.

Challenges

Complex criteria, evolving delegated acts, and dependency on supplier data are common obstacles.

4. California SB 253 (Climate Corporate Data Accountability Act)

SB 253 introduces mandatory climate disclosure requirements for large companies operating in California, including many publicly traded companies that are already subject to climate disclosure regulations.

What it requires

- Annual public reporting of Scope 1, Scope 2, and Scope 3 emissions following the Greenhouse Gas Protocol.

- Third-party assurance is aligned with phased assurance levels.

Who must report

Companies with more than $1 billion in annual revenue doing business in California. This includes many global organisations headquartered outside the United States.

Why it matters

SB 253 is one of the first laws in the US to require full-value chain emissions reporting, including Scope 3.

Challenges

Scope 3 quantification, supplier engagement, data estimation methodologies, and assurance preparation.

5. CSDDD (Corporate Sustainability Due Diligence Directive)

CSDDD aims to improve human rights and environmental due diligence across global value chains by enhancing sustainability efforts and managing ESG risks throughout business operations.

What it requires

- Identification, prevention, mitigation, and remediation of adverse impacts.

- Integration of due diligence into policies and risk-management systems.

- Development of climate transition plans.

- Public reporting on due diligence processes and outcomes.

Who must comply

Large EU companies and non-EU companies with significant revenue and presence in the EU.

Why it matters

CSDDD shifts responsibility from disclosure to ongoing due diligence action. It intersects with CSRD because due diligence performance feeds into ESRS disclosures.

Challenges

Value-chain mapping, risk scoring, documentation, organisational oversight, and supplier engagement.

6. California SB 261 (Climate-Related Financial Risk Act)

SB 261 is designed to improve transparency around climate-related financial risks, particularly impacting the financial sector and aligning with global standards for climate-related financial disclosures.

What it requires

The law draws on recommendations from the Task Force on Climate-related Financial Disclosures (TCFD), a leading force on climate-related reporting, to guide organisations in assessing and disclosing climate risks and opportunities.

- Biennial climate-risk reports aligned with TCFD and ISSB guidance.

- Disclosures on governance, risk processes, strategy, and financial exposures to physical and transition risks.

Who must report

Companies with over $500 million in annual revenue doing business in California.

Why it matters

It brings climate-risk reporting into the mainstream for US-based and global companies.

Challenges

Scenario modelling, quantifying financial implications, and linking climate risks to enterprise risk management.

7. SFDR (Sustainable Finance Disclosure Regulation)

SFDR governs sustainability disclosures for financial market participants in the EU and is influenced by international standards set by organisations such as the Financial Stability Board.

What it requires

Firms must report on ESG factors and make ESG disclosures at both the entity and product levels.

- Entity- and product-level disclosures.

- Reporting of Principal Adverse Impact (PAI) indicators.

- Classification of funds as Article 6, 8, or 9 with specific reporting expectations.

Who must report

SFDR applies to EU-based asset managers, funds, and financial advisers, as well as certain non-EU managers marketing financial products in the EU.

Why it matters

SFDR shapes investment flows and is closely linked with both the EU Taxonomy and CSRD, creating a data dependency chain from corporates to financial institutions.

Challenges

Interpretation of PAI indicators, reliance on portfolio-company data, and adapting to regulatory updates.

8. EU Deforestation Regulation (EUDR)

EUDR aims to ensure that commodities placed on or exported from the EU market are deforestation-free.

What it requires

- Geolocation data for relevant commodities and products.

- Due diligence statements demonstrating compliance.

- Risk assessments and mitigation measures.

Who must report

Operators and traders dealing in covered commodities such as palm oil, soy, cattle, cocoa, coffee, rubber, and timber.

Why it matters

The regulation raises expectations for value-chain traceability and environmental due diligence.

Challenges

Collecting geolocation information, verifying supplier practices, and integrating traceability systems.

9. Invest Europe ESG Reporting Guidelines (voluntary)

The Invest Europe template is widely used in the private equity and venture capital sector as an example of voluntary ESG reporting frameworks.

What it provides

The guidelines help firms structure their ESG disclosures, support ESG initiatives, and facilitate ESG reporting within mainstream corporate reports, such as annual reports.

- Standardised ESG templates and KPIs for portfolio companies.

- Guidance for fund-level and firm-level reporting.

- Voluntary alignment with EU sustainability policies.

Who uses it

Private equity firms, venture funds, and LPs investing in European markets.

Why it matters

It improves interoperability between SFDR, EDCI and CSRD frameworks and provides a comparable baseline for ESG data in the European private markets. As a Supported Technology Vendor, KEY ESG enables seamless integration of the Invest Europe ESG template to streamline data collection and reporting.

Limitations

As a voluntary framework, it does not carry legal enforcement. However, it does reflect industry expectations.

10. Taskforce on Nature-Related Financial Disclosures (TNFD) (voluntary)

The TNFD is a task force focused on nature-related financial disclosures. TNFD provides a framework for assessing nature-related impacts, risks, and opportunities.

By addressing nature-related risks and opportunities, TNFD's work supports the transition to a sustainable future, helping organisations make informed decisions that benefit both society and the planet.

What it requires

- Application of the LEAP methodology: Locate, Evaluate, Assess, Prepare.

- Analysis of nature dependencies and impacts.

- Disclosure structure mirroring TCFD: governance, strategy, risk, metrics, and targets.

Who uses it

Companies and financial institutions are preparing for emerging nature-reporting regulations or investor expectations.

Why it matters

Nature-related risks - such as water scarcity, land degradation, and biodiversity loss - are rising on regulatory and investor agendas.

Challenges

Limited data availability, new metrics, and integration of nature factors into risk frameworks.

What do these frameworks mean for reporting teams?

The expansion of ESG regulations increases the need for coordinated workflows across sustainability, finance, procurement, and risk teams. Several themes are consistent across the ten frameworks:

- Wider value-chain expectations: CSRD, CSDDD, EUDR, SB 253, and SFDR all depend on high-quality supplier or portfolio-company data.

- Climate becoming mandatory: IFRS S2, AASB ASRS, SB 253, and SB 261 push climate disclosures into mainstream reporting.

- Scenario analysis and transition plans: These are now required or strongly recommended across multiple frameworks, increasing modelling and forecasting needs.

- Audit and assurance: CSRD, SB 253, and future ISSB implementations raise the bar for documentation, traceability, and controls.

- Interoperability challenges: Organisations must understand how one framework feeds another, for example, CSRD data supporting SFDR, or ISSB aligning with TCFD.

These developments make it essential to centralise data, standardise processes, and maintain reliable audit trails.

How KEY ESG helps organisations meet global reporting requirements

Growing regulatory complexity increases the need for integrated systems. As a leading ESG software, KEY ESG supports organisations across all major global reporting requirements.

Collect

- Centralised ESG and carbon data across departments and geographies.

- Support for GHG Protocol methodologies and 70,000+ emission factors from DEFRA, US EPA, and Climatiq.

- Supplier and value-chain data collection tools.

Comply

- Structured workflows aligned with CSRD/ESRS, ISSB/AASB, EU Taxonomy, SFDR, EUDR, SB 253, SB 261, and TNFD.

- Coverage of mandatory and voluntary frameworks with compliance support built in.

Report

- Automated disclosure outputs, audit-ready evidence logs, and version control.

- Templates aligned with key frameworks for faster reporting cycles.

Improve

- Insights into performance trends, risk exposure, and reduction opportunities.

- Support for transition planning and scenario modelling.

Carbon Accounting

- Full Scope 1–3 coverage aligned with the GHG Protocol.

- Transparent methodologies and automated audit-trails of emission factor calculation.

Moving forward with confidence in ESG reporting

ESG reporting is accelerating globally, driven by regulatory mandates, investor expectations, and market pressures.

As these frameworks continue to converge, having robust, scalable systems becomes essential. A robust sustainability strategy is crucial for long-term success in ESG reporting, helping organisations set clear goals, demonstrate accountability, and drive sustainable development.

Request a demo to see how KEY ESG streamlines ESG data collection, verification, and reporting - giving your organisation confidence across every global framework.

.png)

.avif)